Payout System Guide: Key Tradeoffs to Know in July 2026

A lot of teams treat their payout system choice as a one-time setup task. It rarely stays that way. Once your volume grows, questions about payout account settings, payout settlement speed, prepaid payouts card programs, and open class action settlements disbursement start stacking up fast. And if you're paying across borders, an international payout system with the wrong rails can quietly eat your margins on every transfer. This guide walks you through the real tradeoffs so you can build a payout account setup you won't need to redo in six months.

TLDR:

- A payout system routes outbound disbursements to payees; it requires different infrastructure than inbound payment processing.

- Your rail choice controls settlement speed: ACH takes 1 to 3 business days, while RTP and FedNow settle instantly.

- 76% of organizations faced fraud attempts in 2025, making KYC verification a non-negotiable step before funds move.

- The cross-border payments market hit $187.7 billion in 2025, growing to $312.1 billion by 2033 at a 7.1% CAGR.

- Dots routes $1.5 billion annually to over 1 million payees across 190+ countries via 300+ payout methods.

What a Payout System Is

A payout system is the infrastructure that routes your outbound disbursements to payees, including contractors and insurance claimants. Inbound processing collects money at checkout, but sending funds outward relies on completely different tech.

Why Outbound Rules Differ

Collecting money focuses on authorizing a transaction. Sending money via a payout system introduces new structural hurdles:

- Verifying payee identity against KYC requirements to block fraudulent recipients before funds move. Tax compliance adds another layer: collecting W-9s (US tax identification forms) from US payees and W-8BENs (foreign status certification forms) from international recipients before any disbursement processes. Rail selection then determines whether funds settle in seconds via RTP or FedNow, or in one to three business days via ACH (Automated Clearing House).

How Payout Systems Work

A completed job or approved insurance claim initiates the sequence. Once authorized, the payout system executes specific steps to move funds outward:

- Information collection captures recipient details securely when users access their payout account login.

- Identity verification runs mandatory KYC (Know Your Customer) checks against global watchlists before money moves.

- Routing logic checks the payee location and preferred payout account settings to select the correct rail: ACH for domestic transfers, RTP or FedNow for instant settlement, or SWIFT and local rails for international payees.

- The system initiates the transfer and generates a timestamped record for every disbursement.

- For cross-border payments, currency conversion applies before funds leave, with fees determined by the provider's FX model.

Types of Payout Systems

Choosing the right payout system depends on your exact category of tech. Knowing the difference between consumer apps and enterprise APIs determines how payees access their money.

- Bank transfer networks route funds directly to checking accounts via ACH payment clearinghouses.

- Digital wallets fund a payout wallet directly. Users use a payout login to check their payout account balance or move money.

- Prepaid card programs issue physical or virtual cards loaded with funds, giving payees instant purchasing power without a bank account. This model works well for gig workers, insurance claimants, or any payee who needs immediate access to earnings. Cards can be reloaded via API, and spending controls let businesses restrict where and how funds are used.

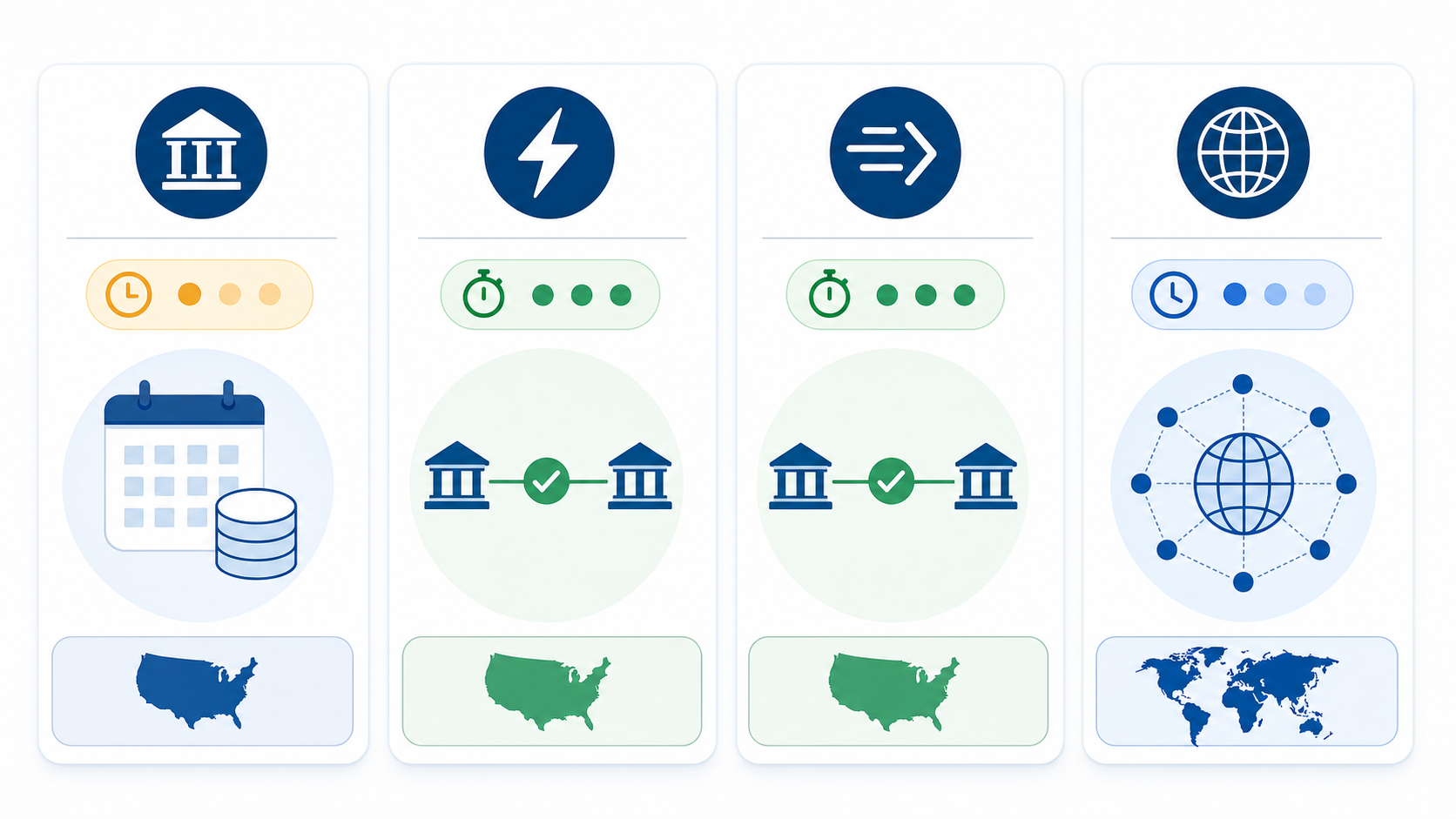

Key Payment Rails: ACH, RTP, FedNow, and SWIFT

A payout system relies on underlying networks to route capital. Your choice of rail controls how fast payees receive money and what you pay to send it.

ACH

The standard domestic Automated Clearing House (ACH) rail operates on a batch-based cycle. Funds settle within one to three business days.

RTP and FedNow

These US real-time payment rails, RTP (operated by The Clearing House) and FedNow (operated by the Federal Reserve), settle funds in seconds, around the clock, every day of the year. Unlike ACH, neither rail batches transactions; each payment clears individually and irrevocably. That finality makes them well-suited for gig workers who need same-day access to earnings or insurance claimants awaiting urgent disbursements. Some providers charge a surcharge of 1 to 1.5% for instant settlement; a flat-fee model keeps those costs predictable regardless of transfer volume.

Rail | Settlement Speed | Processing Model | Geographic Reach | Typical Use Case |

|---|---|---|---|---|

ACH | 1 to 3 business days | Batch-based | Domestic (US) | Standard contractor or vendor payouts where speed is not critical |

RTP | Seconds (24/7/365) | Individual, irrevocable | Domestic (US) | Gig workers needing same-day earnings access |

FedNow | Seconds (24/7/365) | Individual, irrevocable | Domestic (US) | Insurance claimants awaiting urgent disbursements |

SWIFT / Local Rails | Varies by country | Varies by network | International (190+ countries) | Cross-border payouts; jurisdiction-aware routing selects the lowest-cost local rail (e.g., PIX for Brazil, UPI for India, SEPA for Europe) |

Benefits of Using a Payout System

Building outbound payment infrastructure internally drains engineering hours. Adopting an API cuts manual overhead and speeds up settlements. You gain immediate upside over internal builds.

Business Advantages

- Global routing sends capital worldwide without requiring individual banking relationships.

- Disbursement speed accelerates through direct API triggers.

- Payouts automation replaces the daily grind of chasing tax forms.

Payee Experience

While teams sometimes search for a dedicated payout account login or balance portal, the strongest systems embed that experience directly: giving payees a white-labeled dashboard to view earnings, select their preferred payout method, and track settlement status in real time. That transparency reduces support tickets and builds trust. Payees who can see exactly when funds arrive and choose between ACH, instant transfer, or a prepaid card are far less likely to churn to a competitor service.

Common Challenges and Trade-Offs

Every architectural choice carries friction. Implementing a payout system removes manual processing but introduces structural limitations. You must weigh these exact tradeoffs before committing engineering hours.

- Integration complexity slows product launches. Stitching separate tools for KYC checks, tax filing, and bank transfers demands multi-week sprints: a problem that mass payout solutions are built to solve.

- Hidden fees erode margins. Many providers apply heavy FX markups on international transfers or charge premiums for instant rails.

Compliance, KYC, and Fraud Prevention Requirements

Moving funds outward demands a compliant payout system. According to the 2026 AFP Payments Fraud and Control Survey Report, 76% of organizations faced fraud attempts in 2025. Instant networks like RTP and FedNow clear transactions immediately and irrevocably, which means fraud prevention must happen before funds move, not after. A compliant payout system screens every recipient against global watchlists, verifies identity through KYC checks, and matches Taxpayer Identification Numbers against IRS records before any disbursement processes. Skipping these steps exposes you to fraud losses and creates direct regulatory liability under FinCEN (Financial Crimes Enforcement Network) and IRS rules.

International Payout Considerations

The cross-border payments market hit $187.7 billion in 2025 and will reach $312.1 billion by 2033 at a 7.1% CAGR. Scaling an international payout system introduces friction with cross-border payments and currency conversions that can quietly erode margins on every transfer. Many providers apply FX markups of 2% or more on top of the mid-market rate: on a $500,000 monthly payout batch, that's $10,000 lost before payees ever see their funds. Jurisdiction-aware routing solves this by selecting the lowest-cost local rail for each recipient country: PIX for Brazil, UPI for India, SEPA for Europe. You also need to collect the right tax forms, including the W-8BEN for international payees, before any disbursement processes, or risk IRS penalties for non-compliance.

How to Compare and Choose a Payout System

Choosing a payout system requires matching infrastructure to your exact use case. A domestic marketplace needs different mechanics than a nonprofit disbursing global grants. Review these criteria before committing engineering hours:

- Supported rails and country coverage control where funds route globally.

- Settlement speed determines whether payees wait seconds or days, while instant surcharges reduce margins.

- Transparent pricing models eliminate hidden FX spreads, and reviewing Form 1099 and W-8BEN collection requirements is equally critical.

How Dots Powers Payout Infrastructure

We built Dots as an API-first payout system for businesses paying contractors, claimants, and sellers. Today, we route $1.5 billion annually to over 1 million payees.

A unified setup replaces fragmented tools:

- Routes funds through 300+ methods across 190+ countries via global payouts infrastructure.

- Clears transfers via real-time rails, including RTP, FedNow, ACH, and SWIFT, with no instant surcharge for same-day settlement.

- Handles KYC verification, tax form collection, and compliance screening before funds move.

Final Thoughts on Payout System Infrastructure

Building outbound payment infrastructure involves more moving parts than most teams expect: rails, KYC, FX, tax forms, and fraud checks all have to work together. Knowing your use case before you commit to a system saves real time and money. Get in touch with us if you want to see how a unified payout API handles these pieces for you.

FAQ

What is a payout system and how does it differ from payment processing?

A payout system is the infrastructure that routes outbound disbursements to payees such as contractors, sellers, insurance claimants, and grantees. Payment processing collects money inbound at checkout, while a payout system handles the opposite flow, requiring separate identity verification (KYC), tax compliance, and rail routing logic before funds move.

What's the fastest way to set up a payout account for contractors across multiple countries without building custom infrastructure?

Using an API-first payout system like Dots lets you go live in under a week without stitching together separate tools for KYC checks, tax filing, and bank transfers. Dots routes funds through 300+ payout methods across 190+ countries, with real-time settlement via RTP and FedNow at no instant surcharge, and payees set up their own payout account settings through a white-labeled portal.

How do I choose between ACH, RTP, and FedNow for my payout settlement needs?

Choose ACH when cost is the priority and payees can wait one to three business days for funds to settle. Choose RTP or FedNow when your payees need instant access to earnings, since both rails settle in seconds with no extra surcharge on a service like Dots, unlike providers that charge 1.5% for instant transfers.

Can I build an international payout system without taking on FX markup fees?

Yes, but you need to select a provider that uses jurisdiction-aware routing instead of a single fixed rail. Many providers apply FX markups of 2% or more on cross-border transfers; Dots routes each payment through the lowest-cost rail available for the recipient's country across 300+ local rails, including PIX for Brazil and UPI for India, keeping fees transparent and predictable.

What compliance steps does a payout system need to handle before funds can move to payees?

A compliant payout system must collect and verify payee identity through KYC checks, match Taxpayer Identification Numbers against IRS records, screen every recipient against global watchlists, and collect the correct tax forms, including W-9 for US payees and W-8BEN for international recipients, before any disbursement processes.