Paying India's Creators with UPI June 2026

Paying creators in India means managing dozens of routing methods, each with different settlement speeds and fee structures. Your service processes brand sponsorships that should clear in days but stretch to 60 or 120, affiliate commissions that arrive in high volumes of tiny transactions, and cross-border deals that lose 5 to 8% to conversion markups. As of June 2026, UPI moves 66 crore transactions daily with instant settlement and zero fees, yet most creator services can't tap that rail automatically for upi creator payouts. When you scale to thousands of indian influencer payments monthly, the bottleneck moves from moving money to routing it through the right method at the right time.

TLDR:

- UPI clears 66 crore transactions daily in India with instant, zero-fee transfers for creators.

- Indian creators lose 5 to 8% of cross-border earnings to currency conversion and transfer fees.

- Brand sponsorships force 60 to 120 day payment delays instead of standard 30-day terms.

- API payout tools automate KYC verification and route payments under 30 seconds vs 1 to 5 business days.

- Dots supports direct UPI creator payouts and 300+ payment methods under one contract.

How India's Million-Strong Creator Base Earns Money

India houses millions of individuals turning content creation into full-time careers. When you pay creators in India, you encounter diverse revenue models requiring adaptable payout rails.

Top earners secure large brand sponsorships and collect ad splits from video hosting services. Meanwhile, niche creators depend on alternate models:

- Affiliate marketing programs generating high volumes of microtransactions from commission sales

- Paid fan subscriptions requiring recurring local currency payouts for exclusive content access, where creators earn predictable monthly revenue directly from their audience. These subscription models demand reliable settlement infrastructure that handles automatic renewals and processes thousands of small transactions without eating into margins through per-transaction fees.

Creator Earnings by Follower Tier in India

Audience size drives market rates. When you manage indian influencer payments, earning tiers guide your routing logic. Nano creators (under 10,000 followers) make ₹5,000 to ₹20,000 monthly from brand deals and affiliate commissions. Micro creators (10,000 to 100,000 followers) average ₹10,000 to ₹50,000 per sponsored post. Macro creators (100,000 to 1 million followers) command ₹50,000 to ₹5 lakh per campaign. Mega accounts clear ₹10+ lakhs per post.

How YouTube and Instagram Pay Indian Creators

Video hosting services like YouTube distribute structured ad revenue to creators. Because Indian ad rates sit below Western markets, channels monetizing local audiences rely on high view volume to scale earnings. A standard channel secures a ₹20 to ₹150 RPM. This programmatic model generates baseline income tied directly to algorithmic reach.

Instagram relies on a different model. The service offers minimal direct monetization for short-form video. Instead, creators shape their visual content to secure corporate sponsorships. When you route indian influencer payments for these sponsorships, you process manual invoices, skipping automated ad splits entirely.

Payment Methods Used to Pay Indian Creators

Moving funds across borders requires the right financial rail. Consumer services balance settlement speed against transaction fees. When you pay creators in India, four primary routing methods cover the market:

- PayPal serves as the default choice for global transfers. Currency conversion markups of 3 to 5% apply on top of fixed transaction fees, cutting into final earnings on every cross-border payout. Settlement takes three to five business days, and creators must actively withdraw funds to their local bank account before capital is accessible, adding a manual step that delays access to income.

- Domestic agencies route large Indian influencer payments through NEFT or RTGS bank transfer networks. Settlement takes one to two business days and charges transaction fees based on transfer amount. NEFT processes transfers in hourly batches, while RTGS clears transactions in real time but requires minimum transfer amounts of ₹2 lakh. Both methods work well for high-value brand sponsorships but create friction for recurring microtransactions like affiliate commissions.

- UPI routes instant zero-fee transfers for qualifying transactions under ₹1 lakh, making it the preferred rail for high-volume affiliate payouts and fan subscription disbursements. The next section covers UPI mechanics in detail.

- Digital wallets such as Paytm and Razorpay handle smaller creator payouts where creators prefer not to share full bank credentials. Wallet-to-wallet transfers settle instantly but require creators to actively withdraw funds to their bank account, adding a manual step before capital is accessible.

UPI's Role in Indian Creator Payments

The Unified Payments Interface (UPI) functions as India's financial backbone, clearing 66 crore transactions daily. The network executes instant, zero-fee transfers for qualifying transactions below ₹1 lakh, settling funds in under 30 seconds directly between bank accounts. For creator services routing high volumes of affiliate commissions or fan subscriptions, UPI eliminates the per-transaction costs and multi-day settlement windows that make traditional bank transfers uneconomical at scale. Transactions above ₹1 lakh still clear through UPI rails but may incur transparent flat fees set by participating banks.

The Payment Delay Problem Facing Indian Creators

Brand campaigns offer high revenue but create severe cash flow bottlenecks for indian influencer payments. Instead of standard 30-day settlement terms, creators regularly wait 60 to 120 days to receive payment after delivering content. This forces creators to front production costs for equipment, editing software, and location fees while waiting months for reimbursement. Multi-brand creators manage staggered payment cycles across five to ten campaigns simultaneously, with no unified dashboard showing when capital actually arrives. The delay compounds when brands insist on milestone-based approval gates that stretch timelines even further.

Cross-Border Payment Challenges for Indian Creators

Securing global sponsorships expands audience reach. Yet cross-border friction actively erodes these international earnings. Creators collecting foreign ad splits lose 5 to 8% of every dollar before the capital ever hits their bank. Currency conversion markups stack with intermediary bank fees that vary by routing path, creating unpredictable deductions that compound across multiple monthly payouts. Traditional wire transfers add three to five business days of settlement time, forcing creators to plan cash flow around opaque arrival windows. When you route Indian influencer payments through direct local rails instead of correspondent banking chains, you cut both the percentage-based conversion fees and the multi-day settlement delays that make cross-border earnings unreliable.

Tax and GST Obligations for Indian Creators

Routing indian influencer payments requires mapping local tax codes that determine final settlement values. You must account for three primary compliance triggers:

- Creators earning over ₹20 lakh in annual revenue must register for Goods and Services Tax (GST) and apply an 18% charge to their service invoices. Below that threshold, GST registration remains optional unless they sell physical products or run cross-state transactions. Platforms routing Indian influencer payments must collect and verify GST registration numbers for qualifying creators before processing their first payout. This verification step prevents compliance friction during tax filing season and keeps both the service and the creator audit-ready.

- TDS (Tax Deducted at Source) applies when your service pays an Indian creator more than ₹30,000 in a financial year for professional services. Under Section 194J of the Income Tax Act, you must deduct 10% TDS before releasing the payout and deposit it with the government on the creator's behalf. Failing to deduct triggers equal liability on both parties, making automated TDS calculation a non-optional compliance step at scale.

- PAN card collection is required before processing any single payment above ₹50,000 or cumulative annual payments above ₹2.5 lakh to an Indian resident. Without a valid PAN, you must apply a higher TDS rate of 20%, which increases friction and often triggers creator disputes. Collecting PAN during onboarding, alongside GST numbers and W-8BEN forms for cross-border earners, consolidates all compliance verification into one step.

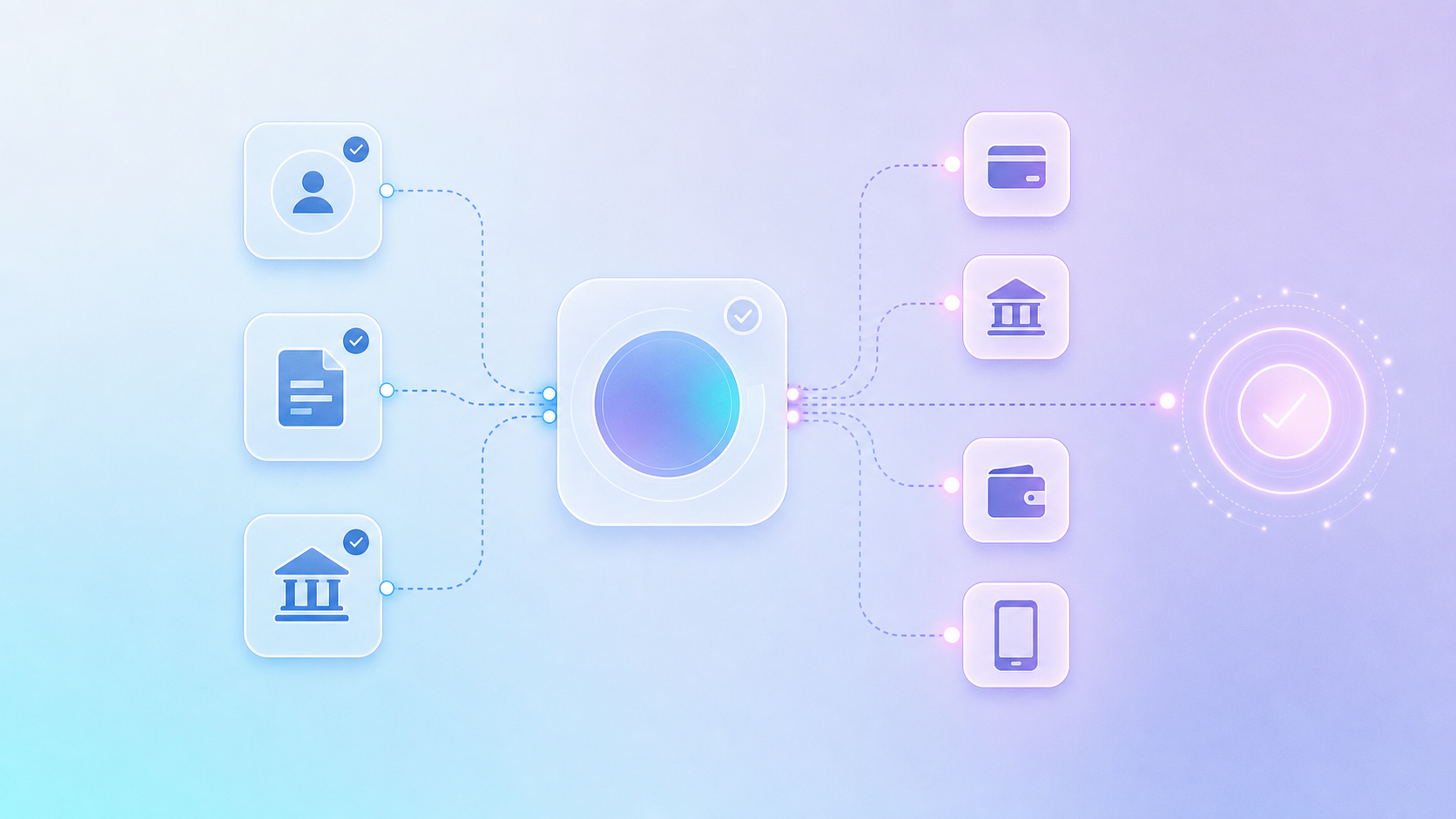

How Payout Infrastructure Works for Creator Services

Feature | Bank Transfers | API Payouts |

|---|---|---|

Settlement | One to five business days | Under 30 seconds |

Compliance | Manual document review | Automated KYC verification |

API-Driven Payouts for Indian Creator Services

Manual work breaks down as your creator count grows. API payout tools let your service trigger payments automatically, handling onboarding, tax collection, and routing through one integration.

We built Dots to give creator services instant capabilities across 300+ payment methods, supporting direct upi creator payouts and digital wallets for indian influencer payments. Under one contract, Dots:

- Verifies identity through automated KYC/KYB checks before the first payout clears

- Collects tax forms (W-8BEN, GST registration numbers) and stores them for audit-ready compliance

- Routes payments through UPI, bank transfers, digital wallets, and 300+ local methods under one integration

- Settles funds in under 30 seconds while tracking every transaction in a timestamped audit trail

Final Thoughts on Scaling Creator Payments in India

When your payout process requires manual bank transfers and 120-day settlement windows, you're competing with one hand tied behind your back. Instant UPI creator payouts and automated compliance checks let you move money the way your creators expect while your team focuses on building product instead of chasing invoices. Get in touch to see what API-driven indian influencer payments can do for your service.

FAQ

Can I pay Indian creators without dealing with cross-border wire fees?

Yes. UPI creator payouts let you settle directly into Indian bank accounts using the Unified Payments Interface, which clears instantly at zero cost for qualifying transactions under ₹1 lakh. For amounts above that threshold or when routing through intermediary banks, you'll pay transparent flat fees instead of percentage-based wire markups.

What's the fastest way to automate Indian influencer payments at scale?

API payout tools deliver instant settlement through 300+ payment methods including UPI, routing funds in under 30 seconds while handling KYC verification, tax-form collection, and compliance checks automatically. Most services go live in under a week, replacing manual CSV uploads and eliminating the 60 to 120-day payment delays common in brand campaign workflows.

How does W-8BEN collection work for Indian creators earning from US platforms?

Indian creators must submit a W-8BEN form before receiving their first payout from a US service. The form certifies their foreign tax status and may reduce the default 30% backup withholding rate on US-sourced income through tax treaty provisions between India and the United States.

Do Indian creators need to register for GST?

Creators earning over ₹20 lakh annually must register for Goods and Services Tax and apply an 18% charge to their service invoices. Below that threshold, GST registration remains optional unless they sell physical products or run cross-state transactions.

UPI vs bank transfer for paying creators in India?

UPI settles in under 30 seconds at zero cost for transactions below ₹1 lakh, while NEFT and RTGS bank transfers take one to five business days and charge transaction fees. For high-volume microtransactions like affiliate commissions or fan subscriptions, UPI cuts settlement time and eliminates per-transaction costs.