1099-NEC for Creators: When Earnings Span 50 States (July 2026)

Filling out a 1099-NEC for creators is one thing. Knowing which states want that data sent directly to their own portals, which ones are already covered through the IRS Combined Federal/State Filing program, and how foreign creators get handled under a completely different withholding regime, that's a different exercise. Creator 1099 multi-state compliance in 2026 requires tracking your payees' resident state, where they physically worked, and your own domicile state, all at once. This breaks down exactly how to do that.

TLDR:

- The OBBBA raises the federal 1099-NEC threshold for creators starting January 2026, but state minimums still apply independently.

- Your service must track 3 jurisdictions per payout: payee residency, work location, and your business domicile.

- NY, PA, and OR require direct portal uploads even when the IRS CF/SF program routes federal data automatically.

- Paying non-US creators triggers a flat 30% withholding under IRC Section 1441 unless a valid W-8BEN is on file.

- Dots routes 1099-NEC compliance, TIN matching, W-9 collection, and international tax forms through one API across 190+ countries.

What 1099-NEC Means for Creator Payouts in 2026

Form 1099-NEC tracks non-employee compensation. For services handling influencer tax filing across jurisdictions, this federal document sets the baseline before state rules apply.

Starting January 2026, the One Big Beautiful Bill Act (OBBBA) raises this standard. The IRS requires a 1099-NEC for creators only when earnings exceed $2,000 in a calendar year, up from the prior $600 threshold. That higher federal floor reduces paperwork for low-volume payees, but it does not eliminate your filing obligations. State thresholds operate independently, and many jurisdictions have not adopted the federal baseline, meaning a $1,500 payout can still trigger a local 1099-NEC requirement even when no federal form is due.

Why Creator Services Face Multi-State Filing Obligations

Paying a creator rarely means dealing with a single local tax agency. Remote distribution triggers a creator 1099 multi-state tax profile, demanding compliance across multiple jurisdictions.

To handle influencer tax filing correctly, your service must track three distinct geographic factors:

- Payee resident state: Local agencies expect a 1099-NEC for creators living in their borders to monitor personal income.

- Physical work location: When a payee travels to shoot a campaign, the state where they perform services claims jurisdiction over those earnings.

- Business domicile: Your company headquarters state requires records of outbound non-employee compensation, regardless of recipient location.

How the Combined Federal/State Filing Program Works

The IRS Combined Federal/State Filing (CF/SF) program cuts redundant paperwork. When you file a 1099 nec for creators electronically, the system routes data to federal and local agencies simultaneously.

How the process works:

- The IRS batches compensation details upon receiving your digital submission.

- The agency forwards records directly to participating state tax departments.

- Paper forms bypass the CF/SF system entirely. Submitting a physical 1099-NEC to the IRS does not trigger automatic forwarding to state agencies. Your team must file separate paper copies directly with each applicable state revenue department, which adds manual work and introduces its own set of state-specific deadlines separate from the federal January 31 cutoff.

States That Require Direct Filing Outside the CF/SF Program

The CF/SF system leaves coverage gaps that trigger late penalties if ignored. Non-participating jurisdictions split into two distinct tracks:

- No filing obligation: Alaska, Florida, Nevada, South Dakota, Texas, Washington, and Wyoming bypass the program completely. With no personal income tax, they require no local information returns.

- Direct portal submission: Revenue departments in New York, Pennsylvania, and Oregon accept federal data but still mandate independent file uploads through local agency sites.

Missing these local rules causes bottlenecks for any service managing a creator 1099 multi-state workload. Your team must isolate direct-file payee locations long before tax season begins.

State Category | States | 1099-NEC Filing Requirement |

|---|---|---|

No personal income tax: no filing obligation | Alaska, Florida, Nevada, South Dakota, Texas, Washington, Wyoming | None: no local information return required |

Direct portal submission required | New York, Pennsylvania, Oregon | Must upload directly to state agency portal even when IRS CF/SF forwards federal data |

Withholding-triggered direct filing | Alabama, Arizona, Minnesota, Utah, West Virginia, Wisconsin | Independent direct upload required only when state income tax is withheld from the payout |

CF/SF participating: no additional action | All other participating states | Federal electronic filing through IRS routes data to state automatically |

State-Level Reporting Thresholds That Differ from Federal

A $1,500 creator payout bypasses the federal $2,000 threshold but still triggers local tax obligations based on residency. State revenue departments set independent 1099-NEC minimums. States conforming to the federal code automatically adopt the new baseline. Jurisdictions with static statutory limits require local legislative amendments to adjust. You must track each payee's resident state threshold as a separate data point, not as a derivative of the federal rule. Some states set their minimum at $600, others lower, and a handful impose no threshold at all, requiring a filing for every dollar paid. Build that per-state threshold table into your compliance workflow before the first payout clears, or a single $1,500 payment can create an unfiled obligation that compounds into a penalty.

Managing State Tax Withholding on Creator 1099s

When your service deducts state income tax from a payee, that exact amount must appear on their final 1099-NEC. This reporting voids automatic Combined Federal/State Filing (CF/SF) coverage, forcing your team to submit records directly to local agencies.

Revenue departments enforce different manual submission rules:

- Alabama, Arizona, Minnesota, Utah, West Virginia, and Wisconsin mandate independent file uploads only when you report local withholding.

- Other jurisdictions demand direct uploads regardless of withholding status.

Local deposit dates rarely match the federal January 31 deadline for a 1099 nec for creators. Missing these local remittance dates triggers financial penalties.

International Creators: W-8BEN, Form 1042-S, and the 30% Default

Paying non-US creators changes your compliance obligations. Under IRC Section 1441, US payers act as withholding agents. You must deduct a flat 30% from US-sourced payments to foreign individuals unless valid documentation exists.

Form W-8BEN confirms foreign status. Collecting it lets payees claim reduced tax rates through international treaties, sparing them the flat 30% default withholding rate imposed under IRC Section 1441. Treaty rates vary by country: a UK creator may owe 0% on royalties, while a creator in a non-treaty country remains subject to the full 30% deduction. Once services complete the payout, you must report those withheld amounts on Form 1042-S and file the corresponding annual Form 1042 with the IRS by March 15. Collect the W-8BEN before the first payment clears, because retroactive withholding adjustments are far more costly than upfront documentation.

Common Multi-State Filing Mistakes Creator Services Make

Mismanaging a creator 1099 multi-state tax profile triggers financial penalties. Procedural oversights in influencer tax filing cause expensive compliance gaps. Services with distributed payees regularly make these specific errors:

- Filing federal returns while skipping local mandates.

- Reporting based on your headquarters instead of the payee's resident state.

- Deducting local income tax without completing the distinct direct-file requirement that withholding triggers. Once your service withholds state income tax from a creator's payout, CF/SF coverage for that payee is voided and your team must upload records separately to the applicable state revenue portal. Skipping that portal submission while still remitting withheld funds leaves a documentation gap that state agencies treat as a late filing, generating penalties on top of the withheld amount already collected.

Step-by-Step Filing Process for Multi-State Creator Payments

Executing a creator 1099 multi-state filing requires strict procedural sequencing. Follow this workflow to complete influencer tax filing without missing deadlines.

- Collect W-9 and W-8BEN tax documents before clearing the first payout to block missing documentation issues.

- Confirm exact payee residency and any physical source state work obligations.

- Check local thresholds and mandatory withholding rules tied to each payee's resident state. Confirm whether that state participates in the CF/SF program or requires a direct portal upload. Note any local deposit deadlines that differ from the federal January 31 cutoff, and flag payees in states with no threshold, because those jurisdictions require a filing for every dollar paid regardless of annual total.

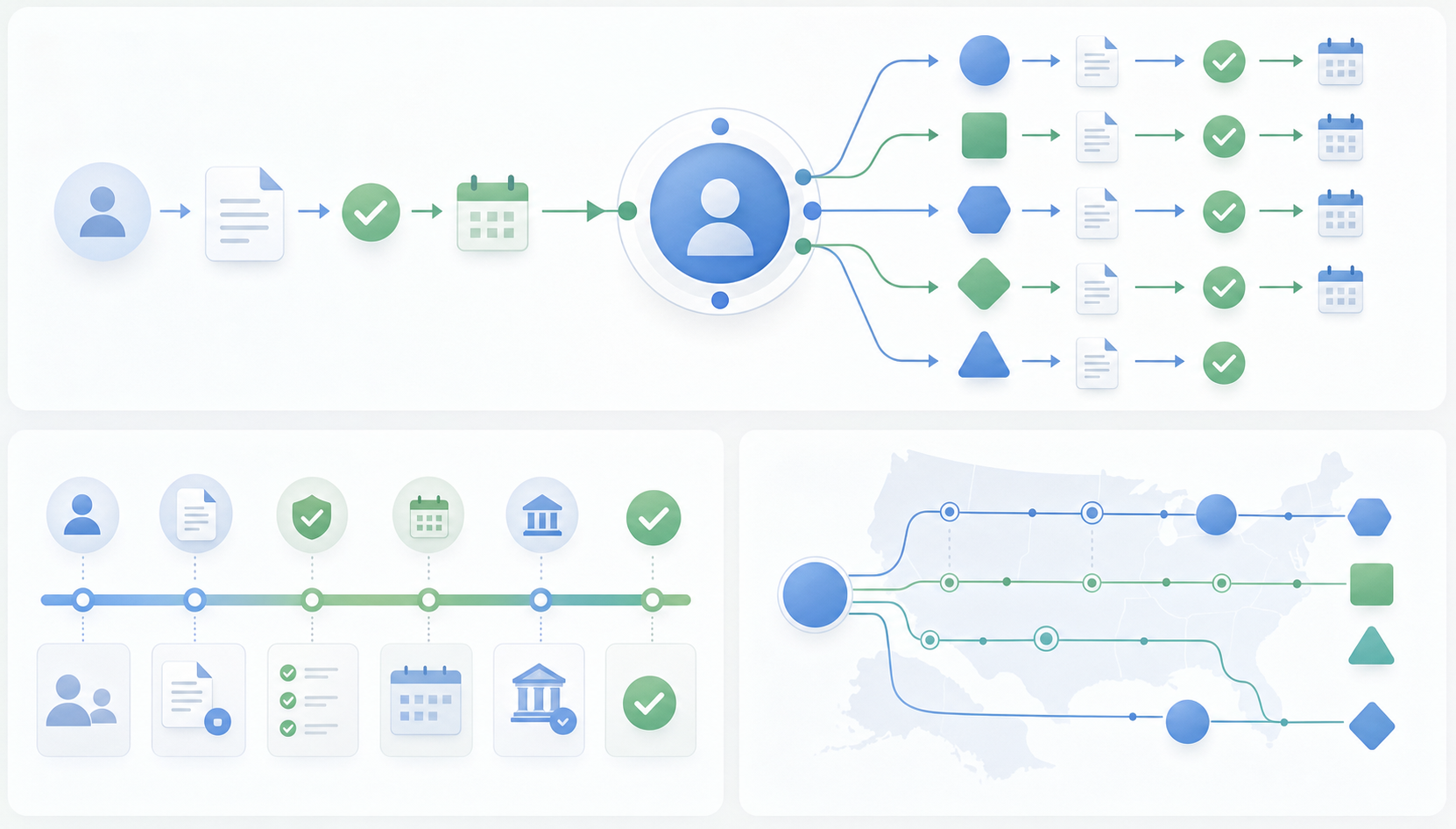

How Dots Automates 1099-NEC, Multi-State, and International Tax Compliance

Managing a creator 1099 multi-state tax profile requires strict oversight. We move $1.5 billion a year to more than 1 million payees across 190+ countries. Your service can automate payouts through one API connection:

- Matches TINs (Taxpayer Identification Numbers, meaning the SSN or EIN used to verify a payee's identity with the IRS) and collects W-9s to generate a 1099-NEC for each eligible creator automatically, with no manual form preparation required. For international payees, Dots collects W-8BEN documentation before the first payment clears and applies the correct treaty-based withholding rate. Direct-file states like New York, Pennsylvania, and Oregon are handled through the same API connection, with records routed to local portals without additional submissions from your team. Every filing deadline, including the federal January 31 cutoff and all divergent state deadlines, is tracked and executed within the system.

Final Thoughts on Creator 1099 and Multi-State Tax Filing

Creator payments rarely stay in one jurisdiction, and that's where most compliance gaps appear. State thresholds differ from federal ones, some states sit outside the CF/SF system entirely, and international creators add a separate layer of withholding obligations. Getting your influencer tax filing workflow right from the start keeps your team out of penalty territory.

Talk to the Dots team to automate 1099-NEC and multi-state filing through one API connection.

FAQ

How do multi-state 1099-NEC filing obligations work for creator services paying influencers across different states?

Your filing obligation follows the payee, not your headquarters. For each creator, you must track their resident state, any state where they physically performed services, and your own business domicile state. Each jurisdiction may independently require a 1099-NEC filing, and some states like New York, Pennsylvania, and Oregon require direct portal submission even when the IRS Combined Federal/State Filing program forwards federal data on your behalf.

What happens if I pay an international creator without collecting a W-8BEN first?

Without a valid W-8BEN on file, IRC Section 1441 requires you to withhold a flat 30% from any US-sourced payment to a foreign individual. Collecting the W-8BEN before the first payout lets the creator certify their foreign status and claim any applicable treaty-based rate reduction, which can bring that withholding rate well below 30%.

How do I handle creator 1099 multi-state filing when my service withholds state income tax?

When your service deducts state income tax from a creator's payment, that withholding amount must appear on the 1099-NEC, and it voids automatic Combined Federal/State Filing coverage for that payee. States like Alabama, Arizona, Minnesota, Utah, West Virginia, and Wisconsin then require independent direct uploads to their own revenue portals, with local deposit deadlines that rarely align with the federal January 31 cutoff.

Should I use Dots or build my own 1099-NEC and multi-state tax filing stack for creator payouts?

Building your own stack means manually tracking per-state thresholds, managing W-9 and W-8BEN collection, running TIN matching, and keeping up with CF/SF participation changes across dozens of jurisdictions. Dots automates TIN matching, W-9 and W-8BEN collection, and 1099 generation through a single API connection that already moves $1.5 billion annually to more than 1 million payees across 190+ countries. The compliance logic is built in, not bolted on.

Can a creator earning below the federal $2,000 threshold still trigger a state 1099-NEC filing obligation?

Yes. A $1,500 payout clears the new federal threshold set by the One Big Beautiful Bill Act but can still trigger a state filing requirement if the creator resides in a jurisdiction that has not adopted the federal baseline and instead maintains its own lower statutory minimum. You must check each payee's resident state threshold independently, as state conformity to federal thresholds requires separate local legislative action.