Scale Automated Payouts Without Adding Headcount July 2026

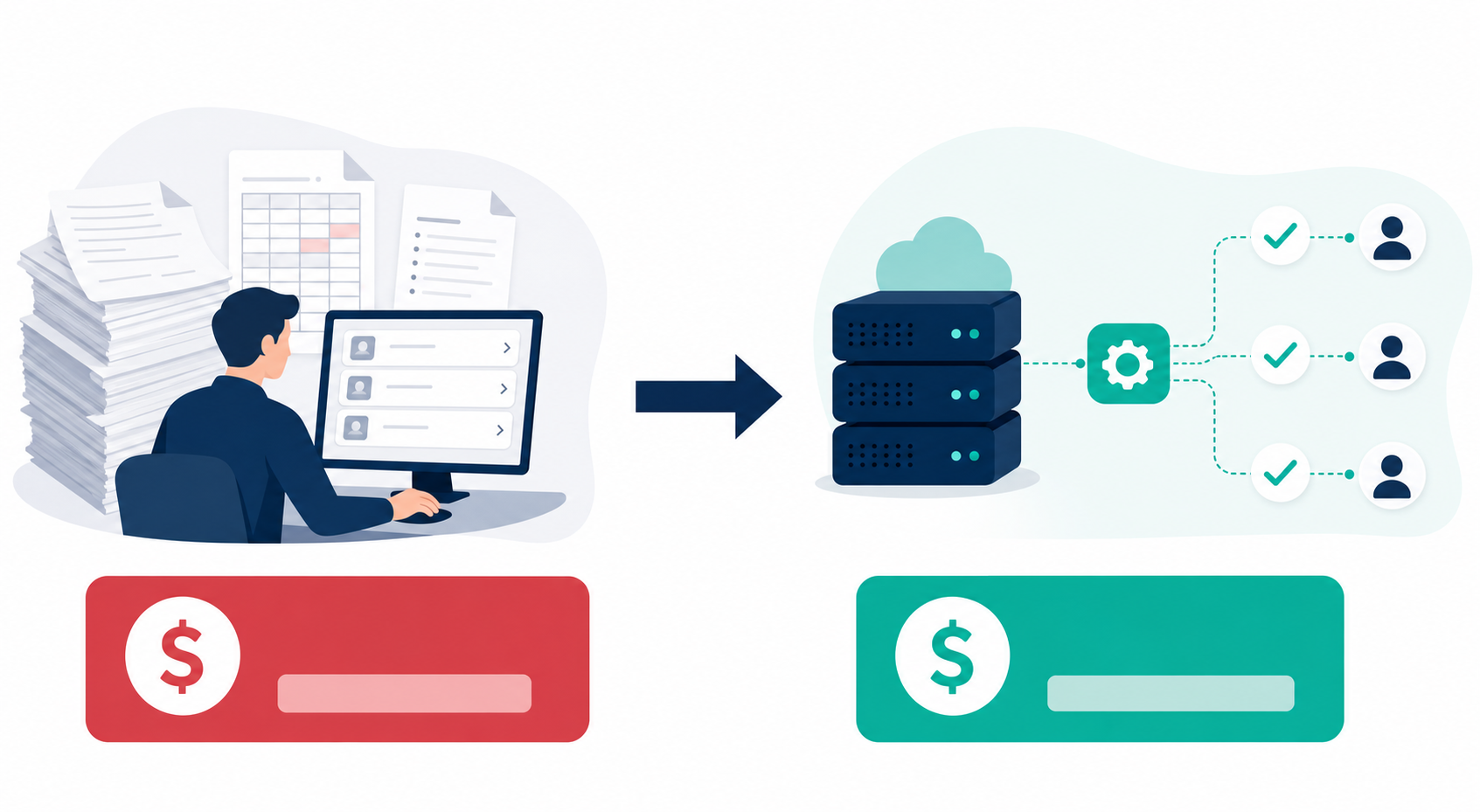

Scaling your payout volume while keeping your team lean is doable, but only if the right things are automated. Most businesses that try this still leave human reviewers in the loop for identity checks, tax collection, or payment approvals, which defeats the purpose. Getting to true automated payouts means wiring up the full sequence, beyond the transfer at the end.

TLDR:

- Manual payouts cost $12 to $40 per transaction (Gartner); automation cuts that figure by up to 80%.

- Automating payouts requires 5 core components: payee verification, trigger logic, rail routing, tax filing, and audit trails.

- Late 1099-NEC filings trigger IRS penalties starting at $60 per form within 30 days of the deadline.

- Audit your transaction volume, identity review process, and rail coverage before switching to automated payouts.

- Dots routes payouts via API to over 1 million payees annually, with integrations completing in under a week.

What Automated Payouts Are and How They Differ from Manual Disbursements

Automated payouts swap human intervention for software logic. When you owe contractors or sellers, an API triggers the disbursement. Code routes the money. The system records transactions directly. Nobody clicks an approval button.

This setup cuts legacy workflows. An automated system replaces:

- Manual bank transfers that invite data errors.

- Offline spreadsheets that demand constant updates.

- CSV uploads requiring human review before each batch run, adding manual bottlenecks that slow disbursements and introduce data-entry errors at scale.

The Hidden Costs of Running Payouts Manually

Manual tasks inflate your baseline cost per transaction. According to McKinsey, businesses cut expenses by up to 30% when they adopt automated payouts. Gartner estimates that manual processing averages $12 to $40 per transaction. Automated tools drop that figure to under $5, sometimes closer to $2, by eliminating approval queues, manual data entry, and human review steps. At high volume, that gap compounds quickly: a business processing 50,000 payouts per month at a $25 manual average spends $1.25 million per month on transaction overhead alone. Automation recaptures most of that cost without adding headcount.

Core Components of an Automated Payout Workflow

A working automated payout system relies on exact building blocks to process volume without human intervention. Break one component, and the sequence stalls. You need these core mechanics:

- Payee onboarding and verification checks identities against global watchlists to block fraudulent accounts.

- Payment trigger logic uses predefined events to move funds automatically, stopping your team from queuing transfers by hand.

- Rail routing matches each transfer to the fastest, lowest-cost network available: ACH, RTP (Real-Time Payments), FedNow (the Fed's instant rail), or an international rail, based on the recipient's location, bank support, and settlement urgency. The system checks these variables per transaction, so high-value or time-sensitive payments move on instant rails while routine batch payouts use ACH to minimize fees.

How to Audit Your Current Payout Process Before You Automate

Map the friction points in your daily workflows before swapping your infrastructure. An internal audit reveals exactly where manual routing slows down capital movement. You need to spot specific bottlenecks before turning on automated payouts.

Audit Area | Core Question | Scale Bottleneck |

|---|---|---|

Transaction Volume | How many payees receive funds per month? | Queuing transfers by hand breaks under high loads. Once monthly payouts exceed a few hundred recipients, manual batching introduces data-entry errors and approval delays that compound at scale. |

Identity Review Process | Who approves KYC documents before funds move? | Human reviewers become the bottleneck. Automated onboarding replaces manual document checks with webhook-triggered verification, blocking disbursements until identity is confirmed without staff involvement. |

Payment Rail Coverage | Which networks does your current stack support? | A single-rail setup creates coverage gaps. Payees in regions unsupported by ACH or wire require a separate workflow, adding manual routing steps that slow settlement and raise per-transaction costs. |

Tax and Compliance Filing | How are 1099s collected and filed at year-end? | Spreadsheet-based TIN (Taxpayer Identification Number) matching and manual 1099 generation create recurring liability. Missed IRS deadlines trigger penalties starting at $60 per form, a cost that scales directly with payee volume if the process stays manual. |

Automating Payee Onboarding and Identity Verification

Moving capital quickly fails if your team reviews identity documents by hand. Many businesses stall here. They set up automated payouts but leave human reviewers to collect tax details and verify identities. Contractor tax compliance and KYC can both be automated: code replaces the manual review step entirely.

Identity verification must finish before funds move. Skipping this step invites compliance fines and opens your system to fraud. An event-driven architecture handles this automatically: a webhook fires when a payee submits their KYC documents, the verification layer checks identity against global watchlists, and the system either unlocks or blocks disbursement access, with no human reviewer in the loop. Tax form collection follows the same pattern, triggering downstream workflows when a W-9 or W-8BEN (Certificate of Foreign Status of Beneficial Owner) is submitted so funds only move once every compliance requirement is confirmed.

Automating Tax Compliance at Scale

Missing IRS deadlines brings heavy financial risk. 1099 tax filing can be fully automated via API, but doing it manually triggers strict IRS penalties:

- $60 per form within 30 days.

- $130 through August 1.

Automated tax compliance works by collecting W-9s and W-8BENs at payee onboarding, before any funds move. The system matches TINs against IRS records throughout the year, catching mismatches while there is still time to correct them. At year-end, it generates 1099-NEC forms based on payment history for every payee who crossed the $600 reporting threshold under IRC §6041, filing on schedule without manual paperwork or missed deadlines.

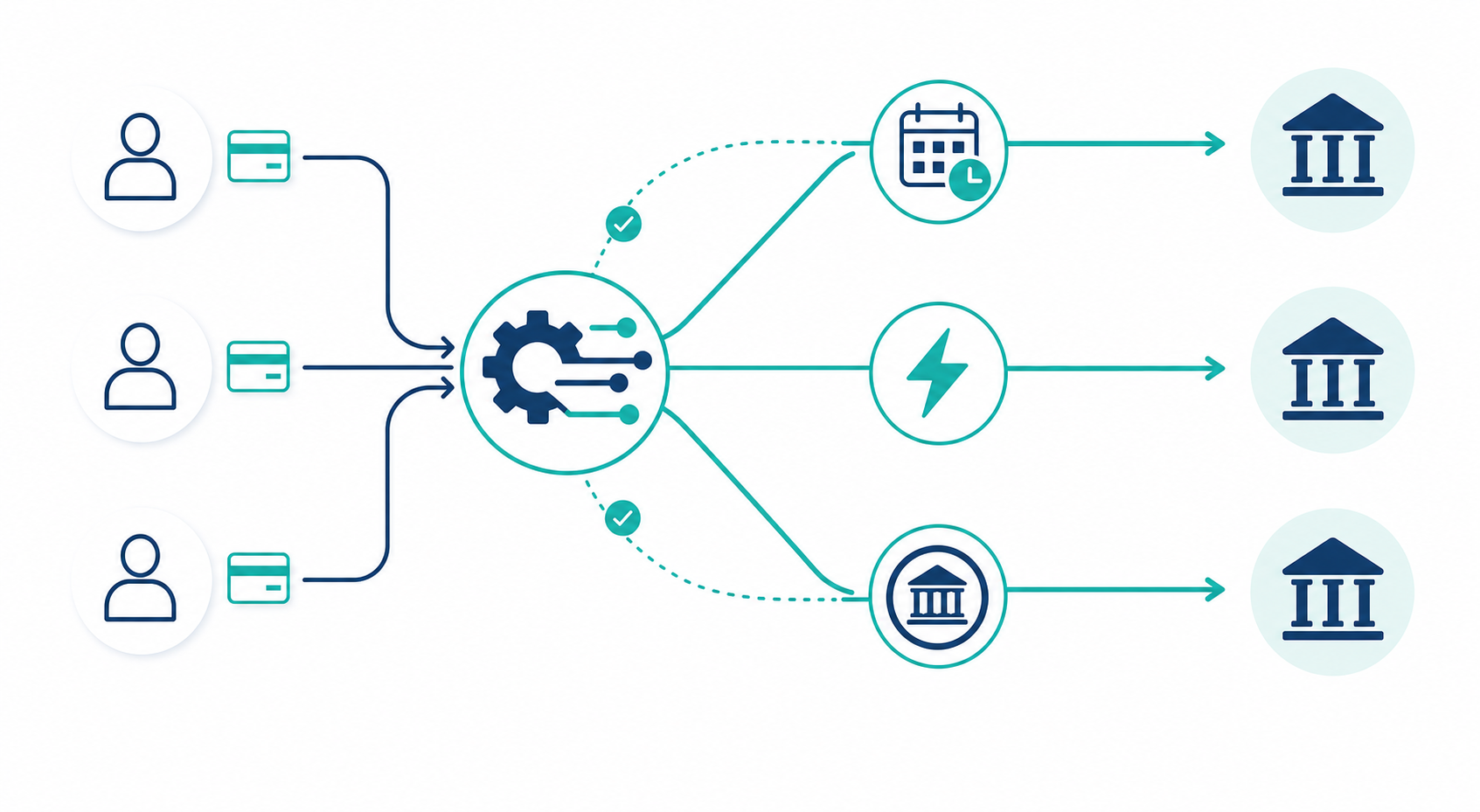

Selecting and Routing Across Payment Rails

Rail selection determines how capital moves. Relying on one network causes coverage gaps and raises costs. Automated payouts scan each transfer to pick the fastest method per jurisdiction.

Automated routing moves US volume away from slow batches using three rails:

- ACH (Automated Clearing House) batches bank transfers for 1 to 5 business day settlement.

- RTP vs FedNow: both act as instant interbank rails with key differences in network coverage and interoperability.

- FedNow settles funds in seconds, 24/7, for time-sensitive disbursements where same-day arrival is required.

How to Integrate Automated Payouts with Your Existing Systems

Connecting new payout infrastructure to your existing tech stack avoids long downtime. Businesses complete a Dots integration in under a week without breaking active operations.

Your available engineering resources determine the path you take:

- API routing connects directly to your codebase, triggering transfers based on specific user actions.

- CSV workflows let business teams process payments via a dashboard, skipping developer queues.

Test the infrastructure in parallel before cutting over fully. Run your new payout stack alongside existing workflows for a defined window (two to four weeks is typical), processing a subset of real transactions through both systems and comparing outputs. Flag any discrepancies in settlement timing, tax-form generation, or webhook responses before decommissioning the old process. Once parity is confirmed, route all volume through the automated system and shut down the manual fallback.

How Dots Handles Automated Payouts Without Adding Headcount

We built Dots as global payout infrastructure delivered as a developer-friendly API. Our system moves $1.5 billion annually to over 1 million payees under a single contract. You scale volume without hiring additional staff because the architecture triggers actions based on strict rules.

Here is what the API executes automatically:

- Gates capital via webhook events until a recipient completes Know Your Customer (KYC) verification. Once identity is confirmed against global watchlists, the system automatically unlocks disbursement access. Tax-form collection follows the same pattern: W-9s and W-8BENs trigger downstream compliance checks before funds move. At year-end, the API matches TINs against IRS records and generates 1099s based on payment history, with no manual paperwork and no missed deadlines.

Final Thoughts on Scaling Payouts Without Manual Work

Once you map the friction in your current process, the gaps become obvious. Manual transfers, human KYC review, and hand-managed tax filings all add cost and risk that compound over time. Automated payouts replace that overhead with rules-based logic your team sets once and your system runs indefinitely. Get in touch and we can walk through the right integration path for your stack.

FAQ

What's the fastest way to set up automated payouts without hiring additional staff in 2026?

The fastest path is integrating a payout API that handles onboarding, compliance, and rail routing under one contract. Dots goes live in under a week using either direct API routing or a CSV dashboard for non-technical teams. Both approaches trigger disbursements based on predefined rules, so no one manually queues transfers or reviews approvals as volume grows.

Can I automate payouts across multiple countries without building separate rail integrations for each one?

Yes. A jurisdiction-aware routing layer automatically selects the lowest-cost rail per recipient country, covering 190+ countries and 300+ payout methods including RTP, FedNow, ACH, Venmo, CashApp, PIX, UPI, and SWIFT. Without this kind of automated routing, your team either hard-codes one rail per region or manually selects methods, which breaks under scale.

How does automated payee onboarding work with Know Your Customer (KYC) verification before funds move?

Automated onboarding uses webhook events to gate payouts until a recipient completes KYC checks: identity verification fires an event that either unlocks or blocks disbursement access, with no human reviewer in the loop. Dots extends this to tax-form collection as well, triggering downstream workflows when a W-9 or W-8BEN is submitted so funds only move once every compliance step is confirmed.

How do I handle 1099 tax filing when running automated payouts at scale?

Automated payout infrastructure like Dots matches Taxpayer Identification Numbers (TINs) against IRS records and generates 1099s at year-end based on payment history, removing manual paperwork. Missing IRS deadlines carries real cost: penalties start at $60 per form within 30 days of the deadline and rise to $130 per form through August 1, so automating this step removes a recurring compliance liability.

Dots vs. Stripe Connect for automated payouts: which handles instant payouts better?

Dots includes real-time rails (RTP, FedNow) at no extra charge, while Stripe charges a 1.5% surcharge for instant payouts and caps fast transfers at $10 million per day. If your payout volume is high or your payees depend on same-day settlement, Stripe's surcharge and daily cap create both cost drag and a hard ceiling that Dots does not impose.